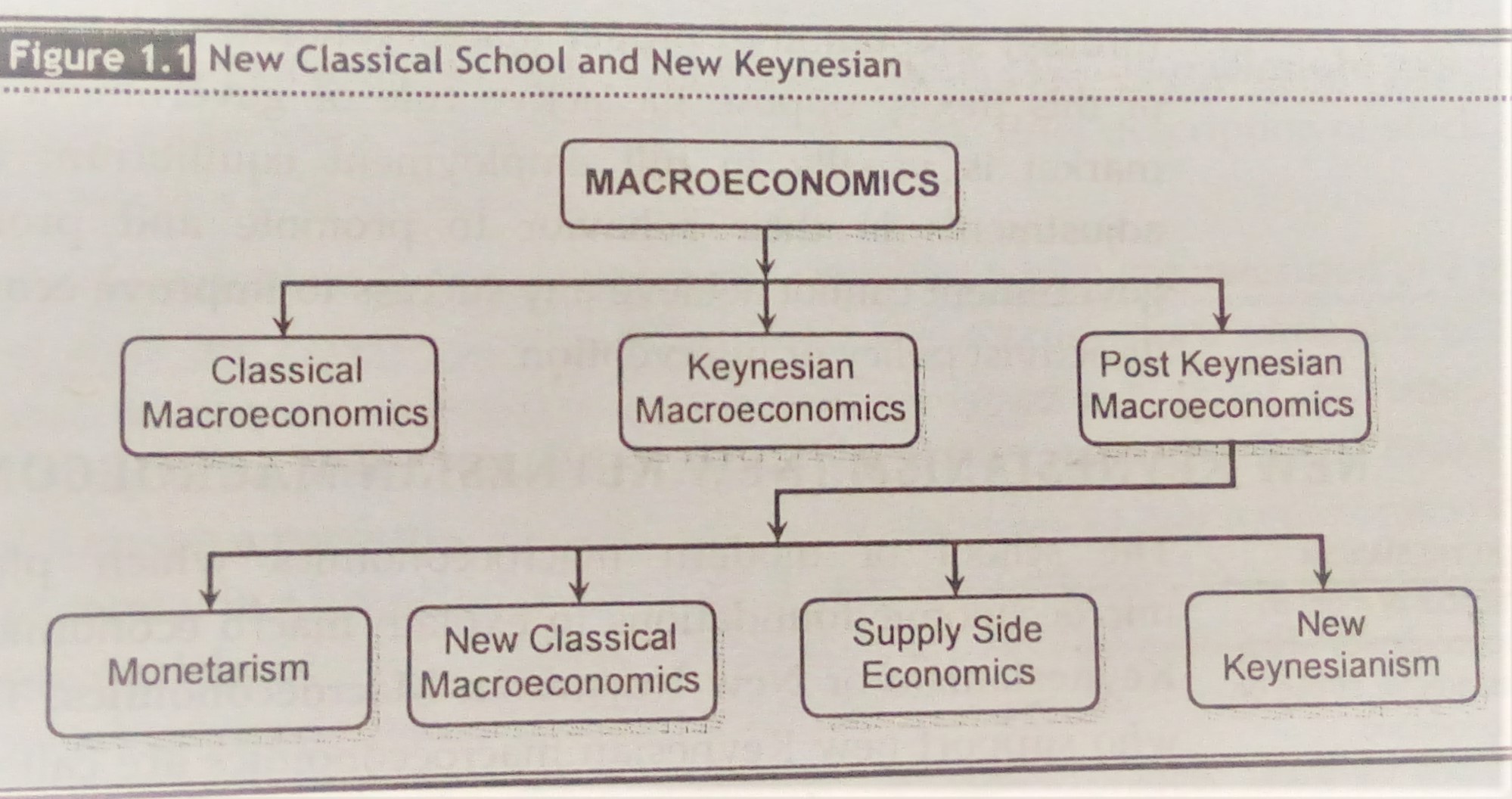

Concept of new classical school and new Keynesian

To understand the concept of new classical school and Keynesianism, we need to understand history of development of macroeconomics thought. The brief history of development of macroeconomics thought is given as follows:

1. Classical Macroeconomics:

The school of macroeconomics thought that dominated the economic world before J.M. Keynes is called classical macroeconomics. Classical economists believed that there would always be full employment in the long run.

2. Keynesian Macroeconomics:

Macroeconomics developed as the separate branch of economics when J.M. Keynes published his book titled “The General Theory of Employment, Interest and Money” in 1936 A.D. before Keynes, classical thought had dominated the economic world. The great depression of 1930s, proved classical basic principle to be wrong; it is because classical economics could not explain the problem created by great depression. Because of such failure of classical economics, Keynesian macro economics was born out of keynes’s attempt to find out solution to economic problems associated with the great depression of 1930s. Keynesian economics dominated the period between late 1930s mid 1960s. this period is also known as the “Keynesian ” period. According to Keynes, level of output and employment is determined by effective demand in the economy and the cause of unemployment is deficiency of aggregate demand in the economy.

3. Post Keynesian macroeconomics:

In the early 1970s, Keynesian economics started showing sign of its failure. Keynesian macroeconomics, especially Keynesian fiscal measures failed to provide solution to economic problems of low economic growth, high unemployment and high rate of return in the developed countries like USA. This led to the growth of new school of macroeconomics thought called monetarism. This school of thought was led by Milton friedman. According to this school, role of money is central to the economic growth and stability, not the role of aggregate demand as Keynes believed. In their opinion, money supply is the main determinant of output and employment in the short and price level in the long run. Monetarism was subsequently followed by the emergence of other schools or thoughts of macroeconomics like new classical school, supply side economics and new Keynesian school. Here we will discuss about New Classical School and New Keynesian Macroeconomics.

NEW CLASSICAL SCHOOL (NEW CLASSICAL MACROECONOMICS)

The new classical school or new classical macroeconomics was developed by the economists like Robert Lucas (Nobel Prize winner of 1995), Thomas J. Sargent (Nobel Prize winner of 2011), etc. against the background of high inflation and unemployment of 1970s. it has presented fundamental challenge to the Keynesian macroeconomics. This school of macroeconomics has its origin in the aspect of classical economics and has same policy conclusion of no government intervention. This school also argus that business cycles occur due to the incomplete information.

The new classical macroeconomics is based on the following three main assumptions:

1. Households and firms make optimal decisions.

2. The expectations are rational. It means that households and firms make correct prediction of the future by using available information.

3. Markets clear, i.e., prices and wages adjust in order to adjust demand and supply.

Among these those assumptions, rational expectation is the main assumption of the new classical macroeconomics. It means that consumers, workers and producers behave rationally to promote their interest and welfare. On the basis of rational expectation, they make quick adjustment in their behaviour. The supporters of new classical school argue that people make correct prediction from the government policies and changes in economic environment. For examples, if central bank of a country increases the money supply, consumers, producers and workers will expect rationally that price level will rise. On the basis these rational expectations, workers would get their wage raised, landlord will raise their rent, bankers increase their interest and producers will raise their profit margins. As a result of these adjustments, effect of expansion of money supply will get cancelled.

New classical economists argues that since consumers, workers and producers themselves make adjustments to save them from the adverse effects of economic events and policies, there is no need for government to intervene in the economy through adaptation of proper macroeconomics policy. Therefore, the supporters of this theory oppose the active role of government and also view that the market is usually in full employment equilibrium an people make self-adjustments in their behavior to promote and protect their interest. The government cannot acheve any success to improve economic situation through its activist policy or intervention.

NEW KEYNESIANISM (NEW KEYNESIAN MACROECONOMICS)

The school of modern macroeconomics which places greater stress on microeconomic foundations to explain macro economic theories is called New Keynesianism or New Keynesian macroeconomics. The group of economists who support new Keynesian macroeconomics are called new Keynesians. This theory was developed in 1980s partly as a response to criticisms against Keynesian macroeconomics by supporters of new classical macroeconomics. The new classical criticisms against the Keynesian macroeconomics were that Keynesian macroeconomics was theoretically inadequate and macroeconomics must be built on a strong microeconomic foundation. The American economists, N.G. Mankiw and David Romar have made important contribution to new Keynesian macroeconomics. The main task of new Keynesians has been to improve microeconomic foundation of the Keynesian macroeconomics and give additional explanation of involuntary unemployment. The group of economists who support new Keynesian macroeconomic are called new Keynesians.

Like the new classical approach, new Keynesian macroeconomic analysis usually assumes that households and firms have rational expectations. They also assume that there is imperfect competition in price and wage setting. Wage and price stickiness, and the other market failures present in new Keynesian models. It implies that the economy may fail to attain full employment. Therefore, they argue that for macroeconomic stabilization and reducing unemployment, the government’s fiscal policy or central bank’s monetary policy can lead to a more efficient macroeconomic outcome than the non intervention policy. However, they tend to favour monetary policy. They also argue that recessions are the result of coordination problems occurred in setting prices and wages.

In spite of several path breaking contributions made to the macroeconomic thoughts over the pasts four decades, Keynesian economy remains central point of reference for schools of macroeconomics either for attack or for its reconstruction. It also appears that macroeconomics is still in the process of developing as a perfect science. Nevertheless, the macroeconomic theories and policies as developed so far have gained wide recognition and application. This gives belief to macroeconomics.

MACROECONOMICS CONCEPTS

STOCK AND FLOW VARIABLES

The economic aggregates used in macroeconomics are called macroeconmic variables. These variables are used to evaluate the performance and to analyse the behaviour of an economy. And the macroeconomics variables are generally grouped under stock variables and flow variables. Brief description of stock and flow variables is given below:

1.Stock Variables:

The macroeconomic variables which are measured at a point of time are called stock variables. In other words, stock variables are the macroeconomic quantities measurable at specified point in time. For examples, the water stored in a tank at a point of time, number of books in a library on a particular date, etc. are stock variables. In macroeconomics, stock of capital in a country, the number of employed persons, money supply, total saving, labour force, business inventories, etc. are measured at a point of time which are some examples of stock variables.

2.Flow variables:

The macroeconomic variables which are measured or expressed per unit of time are called flow variables. In other words, flow variables are measurable only in terms of a specified period of time, i.e., per hour, per week, per month, or per year. For examples, national income, total consumption, total saving, total investment, total export, total import, etc. are flow variables.

EQUILIBRIUM AND DISEQUILIBRIUM

The concepts of equilibrium are used in both microeconomic and macroeconomic analysis. Microeconomics uses partial equilibrium analysis where as macroeconomics largely uses general equilibrium analysis. The brief explanation of equilibrium and disequilibrium is given below:

1. Equilibrium:

In the physical science, equilibrium means balance between opposing forces or forces acting upon each other. In economics, equilibrium refers to a state or situation in which opposite forces, e.g., demand and supply are in balance and there is no tendency of change over a time. In macroeconomics, an economy is said to be in equilibrium when aggregate demand for all capital and customer goods and services in a given period of time and price level. Aggregate supply is the total sum of all capital and consumer goods and service supplied in a given period of time and price level.

2. Disequilibrium:

Disequilibrium refers to the situation in which opposite forces, (e.g. aggregate demand and aggregate supply) are in imbalance. In other words in macroeconomics, disequilibrium refers to situation in which aggregate demand and aggregate supply are not equal. The disequilibrium causing factors arise out of the working process of the economy. The working of market economy is governed by such a large number of interrelated and interacting forces that a continuous balance between market forces (demand and supply) cannot be expected. In fact, imbalances between economic forces are a routine matter in a market economy. The reason is that the decision undertaken by millions of consumers, producers, exporters, importers, workers, bankers and the government and their decisions need not to be always coincide. The result could be disequilibrium in the economy.

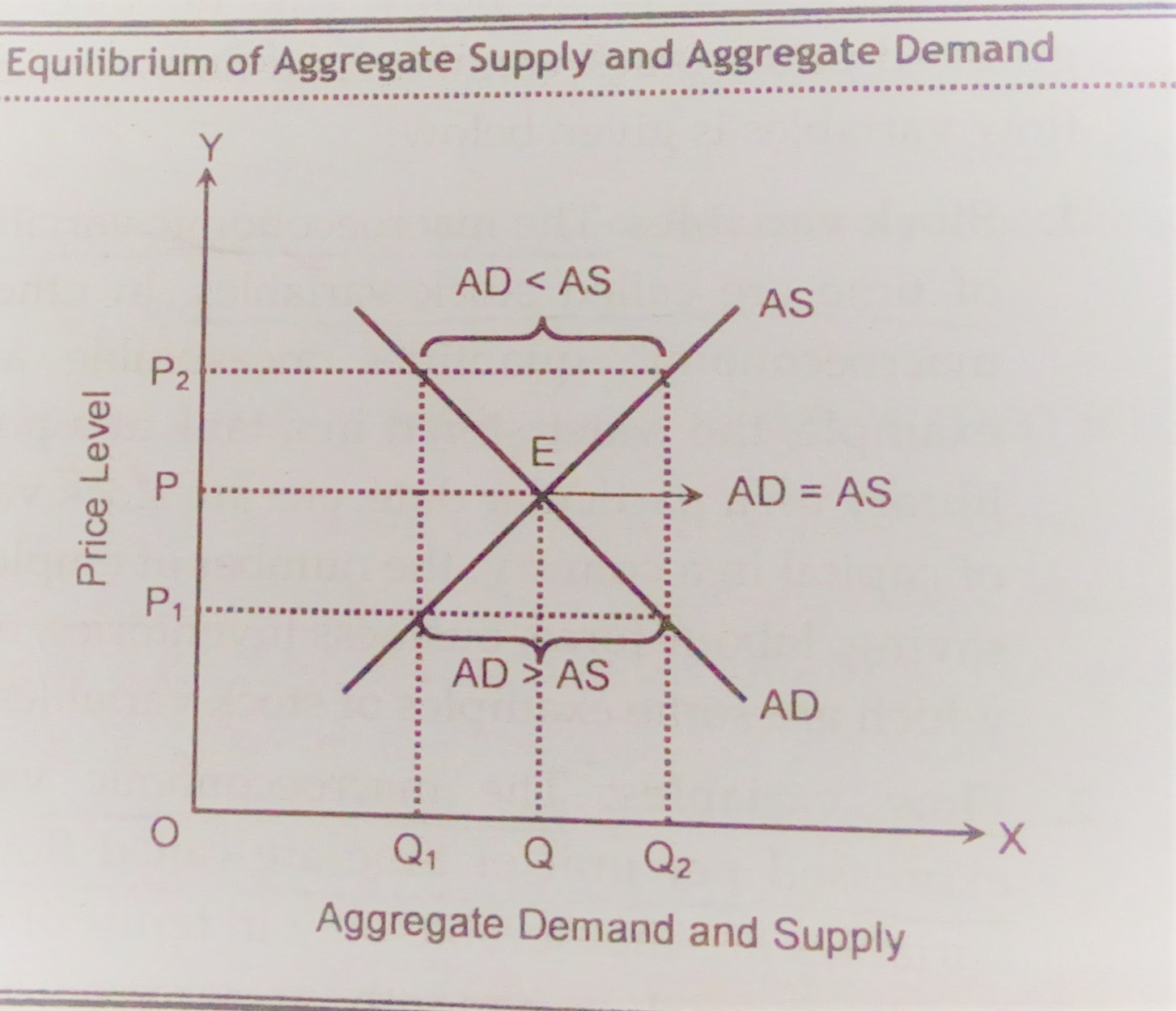

The concept of equilibrium and disequilibrium can be explained by the help of the figure

In the figure, x-axis represents aggregate demand and aggregate supply and y-axis represents price level. The downward slopping curve AD is aggregate demand curve. It is slopping downward because of negative relationship between aggregate demand and price level. The upward slopping curve AS represents aggregate supply curve. It is slopping upward because of positive relationship between aggregate supply and price level. These two curves are intersecting each other at point E. the point E is the equilibrium point. Hence, equilibrium price level is OP and equilibrium quantity is OQ. At any price level above or below OP, there is disequilibrium. In these situations, aggregate demand and aggregate supply are not equal. At any price below OP (say OP1) aggregate demand exceeds aggregate supply. On the other hand, at any price level above OP (say OP2), aggregate supply exceeds aggregate demand.

STATIC, COMPARATIVE AND DYNAMIC ANALYSIS

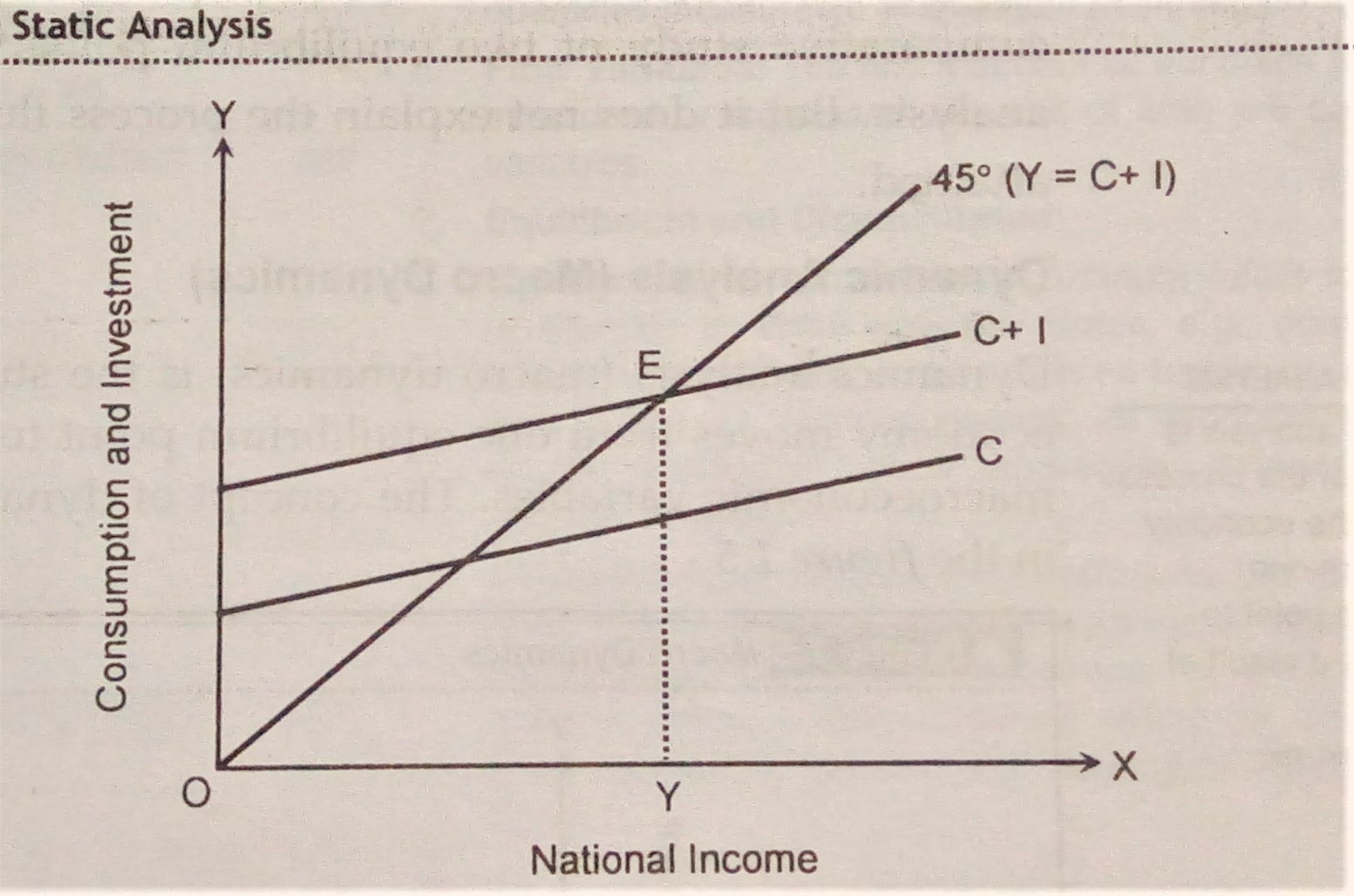

Static analysis (macro ststics)

Static analysis (macro statics) explains the final position of equilibrium of the whole economy at a particular point of time. It shows a still picture of the economy as a whole. It also investigates the relation between macro variables in the final position of equilibrium. But it does not tell the process of adjustment to the final equilibrium. The following equation reflects the final position of equilibrium.

Y=C+I

Where,

Y= Aggregate income

C= Aggregate consumption

I= Aggregate investment

The concept of static analysis has been illustrated in the figure.

In the figure, aggregate demand curve (C+I) and aggregate supply curve (45 degree line) are intersected at point E. point E is the equilibrium point where the equilibrium level of national income is OY. As aggregate demand and aggregate supply refer to the same point of time, it is static analysis.

Comparative analysis (Comparative macro statics)

Comparative analysis (comparative macro statics) is concerned with a comparative study of different equilibrium positions attained by the economy as a result of change in macroeconomic variables. It compares the new and old equilibrium attained by the economy. But it does not deal with the transitional period and process involved in the movement from one equilibrium point to another.

The concept of comparative analysis has been illustrated in the figure.

In the figure, E is the equilibrium point where aggregate demand curve (C+I) and aggregate supply curve (45 degree line) are intersected. OY is the equilibrium level of national income. When there is an increase in investment, the aggregate demand curve shifts to C+I+ change in I. consequently, the new equilibrium point is E1 and new equilibrium national income is OY1. The comparative study of two equilibrium points E and E1 is called comparative analysis. But it does not explain the process through which new equilibrium is attained.

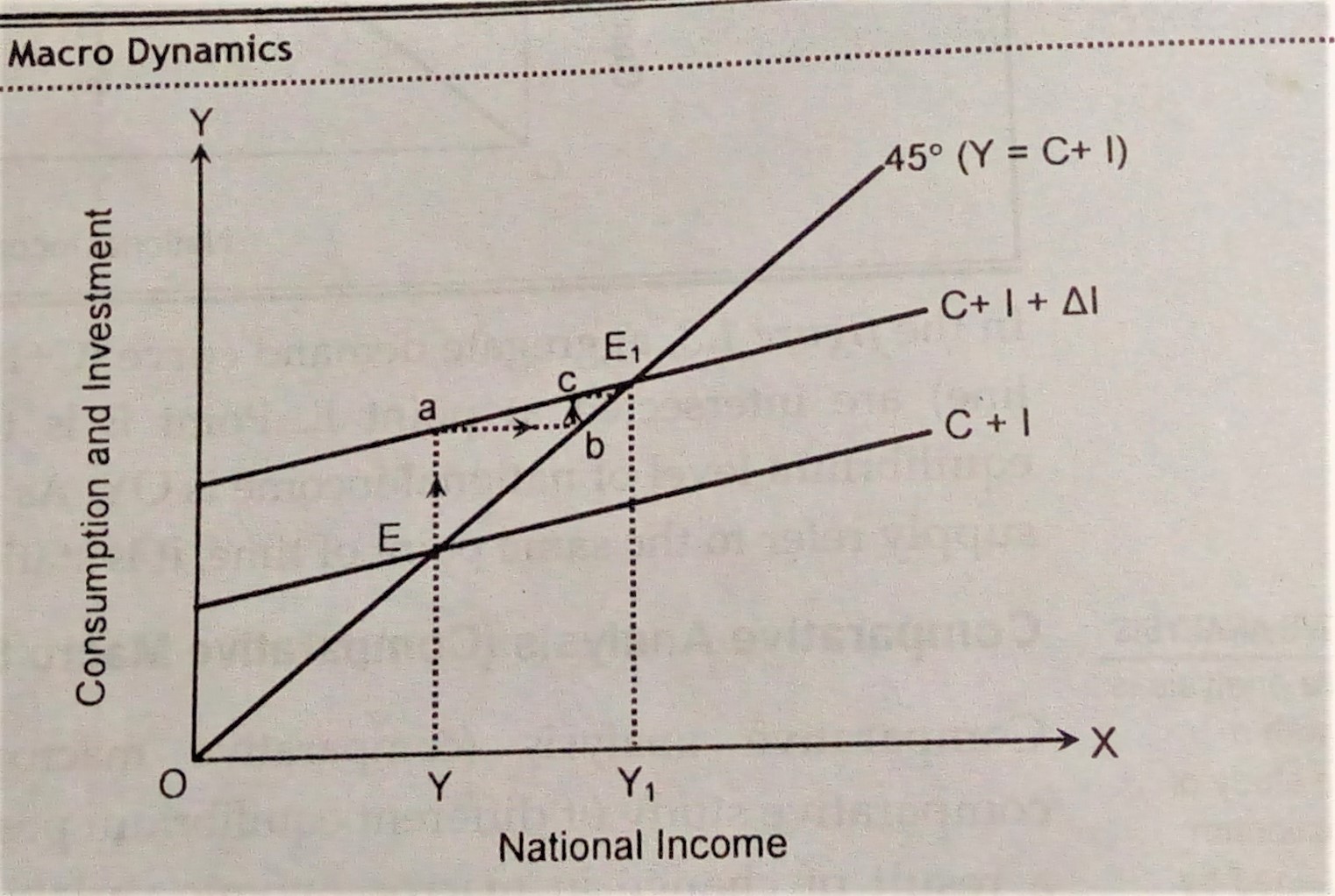

Dynamic analysis (macro dynamics)

Dynamics analysis (macro dynamics) is the study of the process by which the economy moves from one equilibrium point to another as a result of change in macroeconomic variables. The concept of dynamic analysis has been illustrated in the figure.

In the figure, initial equilibrium point is E where the level of national is OY. With the increase in investment, initial equilibrium shifts from E to E1 and level of income increases from OY to OY1. When income increases due to increase in investment, consumption demand also increases. This further increases investment to meet the increased demand. So, the income goes on increasing till the final equilibrium is reached at E1 through the path a,b and c.