Accounting Equation

The accounting equation is also called the balance sheet equation. It represents a mathematical expression of the balance sheet of a business. Therefore, the accounting equation is the equality between the total assets and the total capital and liabilities of the business.

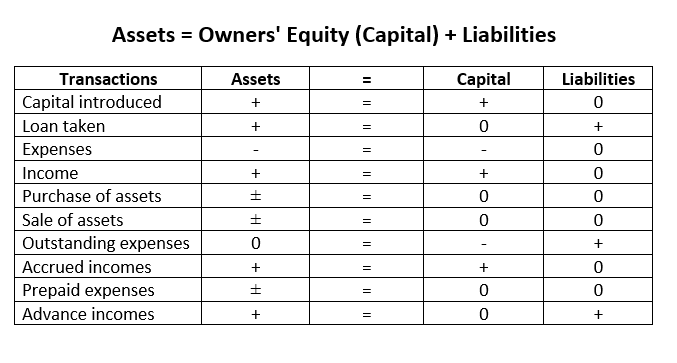

Mathematically,

Every business needs resources to purchase assets to conduct operations. The business acquires those assets from the sources supplied by its owners. The sources supplied by the owners are called capital or the owners’ equity. Sometimes, the sources are also made available by persons other than the owners. The sources made available by persons other than the owners are called liabilities. Therefore, the assets of the business should always be equal to the sum of its capital (owners’ equity ) and liabilities.

THINGS TO REMEMBER (TTR)

The accounting equation is the equality between total assets and the total capital and liabilities of the business. Mathematically,

Assets = Owners’ Equity (Capital) + Liabilities

ACCOUNTING PROCESS OR CYCLE

Accounting consists of a number of sequential steps of activities. These include identifying, recording, classifying, summarizing, and communicating financial transactions. The sequence of the steps to be followed in accounting activities is known as the accounting process. The accounting process takes the form of a cycle. The sequential steps of accounting activities are taken in a cyclical order. The cyclical order starts from the beginning of financial transactions till financial results are derived by preparing final accounts at the end of the accounting year. This cycle follows the same order every year. The accounting process or the cycle is depicted in the following diagram

The accounting process or cycle has the following five steps.

- Identifying the financial transactions: A business may perform several transactions. of which, only financial transactions are recorded in accounts. In the first step of the accounting process, therefore, financial transactions are identified. Financial transactions are those transactions that are expressed in monetary terms.

- Recording of financial transactions: In the second step of the accounting process, all financial transactions performed by the business are systematically recorded in the journal, and subsidiary books. The journal is a book of daily records of financial transactions. Such financial transactions may include cash bills, invoices, bank pay-in slips, and so on.

- Classifying financial transactions: In the third step, financial transactions are classified mainly into the transactions related to persons that include enterprises, persons, assets, and income expenses. Then, they are recorded in their respective ledgers accounts, such as debtors’ and creditors’ accounts, land and building accounts, commission received account, and rent account.

- Summarizing financial transactions: All financial transactions are summarized in the step. They are summarized by preparing a trial balance. The trial balance is a statement of debit or credit balances of all the ledger accounts. Preparation of trial balance helps to prepare final accounts. The final accounts disclose the profit or loss and financial position of a particular period of a business enterprise.

- Communicating the results of business operations and financial position: In the last step, the results of business operations such as profits or losses and the company’s financial position are communicated to the users. Those users include owners, creditors, and managers who need financial information for decision-making purposes.

THINGS TO REMEMBER (TTR)

The sequence of the steps of accounting activities is known as the accounting process. The following are the steps of the accounting process or cycle.

- Identifying financial transactions.

- Recording of financial transactions

- Classifying financial transactions

- Summarizing financial transactions

- Communicating the results of business operations and financial position

my interst